Blockchain is another buzzword in the cryptocurrency world. In fact, cryptocurrencies cannot exist without the blockchain – it is one of the many things that make cryptocurrencies unique.

A quick Google search of the term ‘blockchain’ will probably yield a definition like this: “Blockchain is a distributed digital ledger of economic transactions.” However, this explanation does little to further our understanding.

What is Blockchain Really?

We believe a better definition of a blockchain should sound like this: “A blockchain is a record of cryptocurrency transactions that are kept and maintained by a global network of computers.” To state it another way, it is a decentralized database of transactions.

Imagine a spreadsheet that is duplicated multiple times and kept on thousands of computers worldwide. Whenever a transaction is made, say in Bitcoin, all the computers (or nodes) update the data on their spreadsheet independently.

All nodes must agree on the validity of a transaction for it to be successful. Furthermore, since the records are shared and available to the public, if something goes wrong, everyone will know. This is the essential concept of a blockchain.

This system is fundamentally different from centralized systems, such as a bank. The bank stores all records on a central server. They are responsible for verifying transactions and securing the network.

With the blockchain, the network is not owned by a central authority nor is it located in a single location. All participants in a peer-to-peer network contribute the processing and securing all transactions.

Still not sure what a blockchain is, let’s take a look at the following analogy.

A Simple Analogy

Let’s say you are playing a board game with four other people. In this particular game, one person is the designated scorekeeper. This person, therefore, represents the central authority trusted with the responsibility of ensuring that all in-game scores are fair and balanced.

As we can see, a system such as this is easy to manipulate. The trusted scorekeeper can easily cheat by changing the scores to his/her advantage.

Now picture another scenario – instead of having one scorekeeper, all 5 participants in the game are allowed to keep score. Each person has a separate scoresheet that they will update simultaneously; the game’s scores have now been decentralized.

At the end of the game, everyone compares their scoresheet (or ledgers) to ensure that the scores were recorded accurately and fairly. If all scoresheets match, then everyone can be confident in the truthfulness of the in-game transactions. In other words, all player have come to a consensus.

In contrast to the centralized game which has one scorekeeper, this decentralized system is difficult to manipulate, since all the scoresheets must match for the scores to be deemed valid.

For cheating to occur, someone would have to magically change all of the players’ scoresheets at the same point in time so that they add up at the end of the game – it is virtually impossible.

How Do Cryptocurrencies Work with the Blockchain?

So let’s take what we learned in the decentralized game example and apply it to cryptocurrencies.

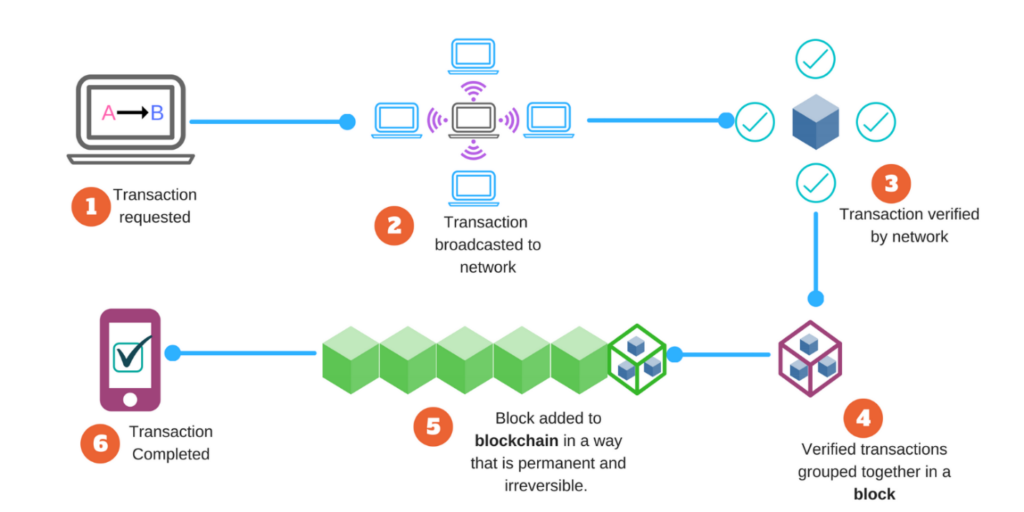

1. A Transaction is Requested

1. A Transaction is Requested

Firstly, say Alice want to send money to Bob. She creates a transaction request which generates a transaction file containing data with the details of the transaction.

2. The Requested Transaction is Broadcasted to the Network

Alice’s transaction is then broadcasted to the peer-to-peer (P2P) network consisting of a global network of computers (nodes). Each nodes has a copy of the distributed ledger. Nodes can be viewed as the individual players in the game with their own copy of the scoresheet.

3. The Transaction is Verified by The Nodes

A number of randomly selected nodes in the network then proceed to verify the transaction by comparing their copy of the ledger to check the following:

- Does the sender have enough money in their balance to do the transaction?

- Is the sender authorized to send the money?

- Is the address receiving the money capable of receiving it?

4. A Block is Created

Once the transaction is verified, it is grouped with a few other verified transactions on the network. This group of verified transactions is known as a block. In the case of Proof of work networks, miners create blocks from a pool of outstanding verified transactions. They then work on solving complex math problems, called cryptographic hash functions, to link their block to the end of the blockchain.

5. The Block is Added to the Blockchain

When the winning miner solves the problem, his/her block gets added to the blockchain. This is then broadcasted to the network where all the nodes update their ledger accordingly.

The result is a transaction that is stored on the blockchain in a way that is permanent and unchangeable. Each block is time stamped and mathematically linked to the other with strong cryptography, making it impossible to hack a block.

5. The Transaction is Completed

Summary:

- A blockchain is a record of cryptocurrency transactions that is kept and maintained by a global network of computers.

- It is decentralized, i.e., it is not owned or operated by a central authority, nor is the network located in a single location.

- A block is simply a group of verified transactions on the network. Each block is linked to the previous one using secure cryptographic hash functions (hence the name ‘blockchain’).